.png)

.png)

.png)

.png)

.png)

Expanding and scaling a business is as risky as they are rewarding. MIT Sloan Management Review finds that the scaling of business endeavor ideation and incubation was only a success among a small percentage of companies (16%). Meanwhile, Igor Buinevici and the Economic Times reported a different finding in which only 8% of organizations were successful in scaling (versus 92% of organizations that failed).

Don’t let these figures stop you from scaling. With ample preparation, a concrete business plan, and organizational alignment, you can scale your business to new heights.

Scaling a business is a calculated risk. As a business owner, it’s important to weigh the pros and cons of scalability before committing to this initiative. While scaling a business improves customer satisfaction and boosts revenue, scaling without sufficient preparation can cost your business.

In a journal article by Saerom (Ronnie) Lee and J. Daniel Kim, the chance of failure rises by 20% to 40% for early-scaling US startup businesses. Scaling within a year (or even six months) of establishing a business is a double-edged sword; it can curb imitation, but it can also lead to market mismatch, poorer brand reputation, and less time for experimentation.

In this case, scaling slower is much more beneficial, but not too slow to the point that you miss out on new market opportunities. How do you know if it’s the right time to scale? Take a look at these five signs.

Increased customer demand for your products and services is a good sign of success. After all, your team has done the hard work of tapping into the needs of your target audience and differentiating your offerings from competitors. However, increased demand comes with the inevitable burden of heavier workloads.

According to the American Psychological Association, half of employees (50%) in the US cited heavy workload as one of the causes of stress in the workplace. If your team is spending the work week rendering overtime or crunching tasks to meet deadlines or targets, it’s a clear sign you need to scale your business through hiring to keep up with the increase in workload.

Employees (63%) leave because there’s no room for career growth. By quitting their jobs, they can negotiate for a higher salary, move out of their comfort zones, and blossom into their careers. If your company’s turnover rates are higher than usual, scaling your business can help retain high-performing talent and promote sustainable growth.

Success doesn’t stop at achieving goals and metrics. If you want to drive operational excellence and business growth, employing a mindset of continuous improvement is a must. This could mean scaling your business to ensure exponential growth and enhanced customer satisfaction. In business, one must not settle for complacency.

You may have the right people and systems to achieve scalability, but having a realistic business plan makes the difference between unexpected costs and a successful scaling endeavor. It helps you stay grounded and accountable for your decisions. So when crafting a business plan, make sure to include concrete ways of scaling your business.

Much like a business plan, a business model is a foundational staple of any company. Business models typically feature your target market, value proposition, metrics, and cost structure.

If your business model has not gained traction yet — or lacks focus and clarity — it’s best to hold off on scaling efforts to avoid risks. But if you have a successful, flexible, and profitable business model, it’s a sign that you can scale your business.

Growth is mesmerizing, but it also blinds business owners. Those who don’t have foresight find themselves in a situation where they are unprepared and ill-equipped to handle the rigors of scaling a business. If scalability is on your radar, take a look at the potential obstacles to business growth you can potentially encounter.

Timing is everything. As discussed earlier, scaling your business too soon sets you up for an increased chance of failure. This is when timing works against you. Before scaling, ask yourself:

Your answers can help you find the right timing to scale your business with minimal financial risks.

Growth and scalability require overcoming a learning curve. Unfortunately, with the talent shortage and high cost of hiring in the US, finding the right people with the specialized knowledge and skills is like finding a needle in a haystack. However, this can be addressed by outsourcing.

Increasing your headcount makes the workload more manageable. But don’t fall into the trap of solely hiring for quantity. Employees are your biggest assets, and one wrong hire can hinder your business’s scalability.

Smart business owners know that scaling initiatives require the right people for the job. While there’s merit in hiring more in-house or outsourced employees, assessing their qualifications, work experience, and skills primes your scaling initiatives for success.

Outdated technology can create inefficiencies in workflow, lower productivity, and put your business at risk of cyberattacks. Investing in new technologies not only helps maintain optimal productivity, it also protects your infrastructure and customers’ data from online threats.

Change can throw teams off guard. It’s recommended to align team members and communicate how each individual’s role and skills contribute to the success of your scaling efforts. Most of all, give your team members a grace period to adjust to the changes and challenges brought by scaling.

Customer needs change as well. In the case of Slack, the company leveraged feedback from app users so it could refine its workplace communication platform with customers’ ever-changing needs in mind. This example shows how adapting to changes can lead to growth and scalability.

Scaling a business can be daunting, overwhelming even. That’s why we put in the work and listed seven scaling business essentials you need to prepare for the next chapter of your organization’s growth.

Failing to plan is recklessness in its purest form. Even if you own a startup, planning ahead helps you anticipate opportunities and threats your business can face as it grows. Make sure your scalability plan includes the following components:

Keep things realistic (but challenging), so everyone can meet the goals and targets outlined in the plan.

Set your sights on your goals and targets. Focus on what your business does best and avoid releasing new products or services without doing deep market research. Failing to conduct market research can result in a poor product market fit that doesn’t target your audience’s needs or attract a new customer base.

When scaling a business, avoid wasting resources on “investments” that don’t serve your customers or contribute to the fruition of your growth strategy.

Business owners need guidance, too. A mentor or consultant can provide sharp, objective insights and opinions without imposing them on you. However, make sure they are the right fit for your company. This means the mentor or consultant has to have the industry knowledge and experience, so they can better help you scale your business.

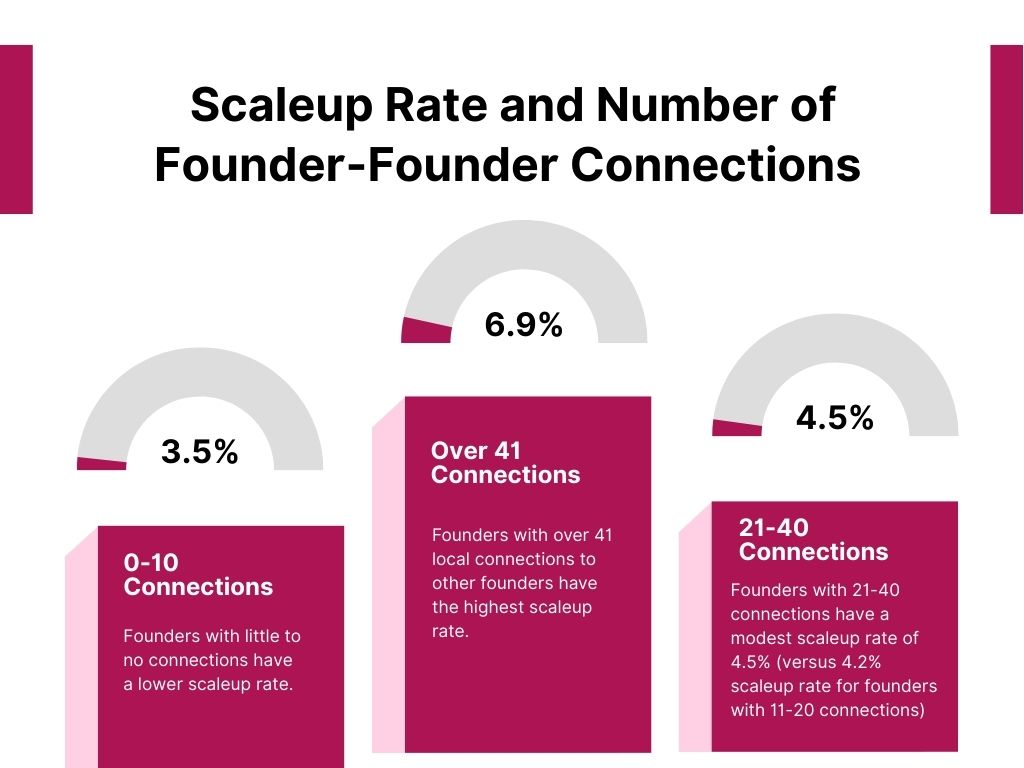

There’s power in networking. In a global study involving 10,500 startup companies, Startup Genome found that founders with over 41 local connections to other founders have a scaleup rate of 6.9%. The scaleup rate decreases if the founder has fewer connections, as exemplified below:

Networking and developing high-quality relationships with fellow founders (or a professional in your industry) give you access to new insights and resources or provide you with opportunities that can make a huge difference in your scaling initiatives. These connections can be potential mentors, too! Hence, always take the “it’s who you know” adage to heart.

While scaling initiatives involve change, it doesn’t mean letting go of core values. Core values are not just for show; they’re your organization’s facade and north star. They keep everyone grounded and create a strong company culture of unity between leaders and employees. Core values also aid in promoting employee retention.

To align employees with company values, start by leading by example so everyone can put these values into practice. Rewarding aligned behaviors also encourages employees to embody your organization’s values for the long haul. Most importantly, integrate core values with scalability efforts and outcomes, enabling employees to gain a sense of purpose and satisfaction when meeting targets.

As you expand your team, hiring the right people becomes a strategic game. Skills and credentials are important, but their shared values and mindset can make a huge difference in hiring decisions. In Qualtrics’ research involving US and UK employees, organizations that don’t demonstrate the respondents’ (46%) personal values can prompt the latter to quit.

Before going on a hiring spree, take the time to understand what your organization is looking for in a candidate to minimize turnover. Think long-term because you’ll want new employees who align with the present and future of your scalability initiatives. Your HR department can filter candidates by asking a mix of standard, behavioral, and situational questions.

Here are some examples:

Scaling your business can make cash flow management trickier than ever before. The solution? Take it by the reins. Start tracking assets, expenses, income, and liabilities using automated cash flow tools. These tools provide a forecast of your cash flow, analyze payment behavior, and predict financial uncertainties, helping you manage your cash flow and prepare appropriate contingency plans, like building a cash reserve.

Balance sheets and other documents also illuminate your business’s financial health. Review them frequently so you can identify risks and areas of growth as early as possible. Just as it is important to expand to new markets and diversify revenue streams, it is likewise important to control expenses through outsourcing and technology.

Not every job function needs to be done in-house. For business leaders, outsourcing is a great way to expedite non-critical work. In a study by Deloitte involving over a hundred executives around the world, the respondents’ rationale for outsourcing was:

This data shows the many advantages of outsourcing. Outsourced teams, in general, are cheaper, so you can expand or downsize your team according to demand and scale without ballooning costs. With service providers handling employee hiring and training, they can source the best candidates, train them in your processes, and prepare them for onboarding in your team.

From cloud-based software to AI and automation, BPO companies boast cutting-edge technologies for whatever need. This speeds up tech innovation and adaptation in your organization while optimizing costs.

The best part about outsourcing is the ability to build a hybrid outsourcing team, allowing you to get the best of both worlds of your in-house and outsourced teams — that is, local knowledge for the former and specialized skills and new perspectives for the latter. This fosters better collaboration between both teams.

It’s important to note that outsourcing can be done within your home country (onshore), a neighboring country (nearshore), or a faraway country (offshore). In terms of cost effectiveness, nearshoring and offshoring are your best bets.

If you decide to offshore outsource, though, you’ll be working with BPO companies in countries with a big time zone difference. That means if you partner with a Philippine-based BPO company, your service provider’s time zone will be 12 to 13 hours ahead of yours. However, time zone differences should not be a hindrance to your partnership.

Scaling a business is a strategic move that, when executed properly, propels your business to exponential growth. If you’re ready to take the next step, start outsourcing your job functions to an outsourcing company.

At KDCI Outsourcing, we offer scalable offshore outsourcing solutions to meet your organization’s growing needs. Carefully vetted by our hiring team, our offshore staff have the expertise to provide world-class outsourcing services that support your organization’s scaling goals and long-term growth. From graphic design to e-commerce, our services cater to various industries.

Build your offshore Filipino team today by getting in touch with KDCI’s outsourcing experts!